AI-Enabled Credit Risk Scoring: The Definitive Guide for Fintech Leaders in the US and UK

Last Updated on: April 16, 2026

How the Systango AI- Native Production Framework™ converts AI experimentation into measurable, auditable profit through AI-Native SDLC, a governed Data Intelligence Layer, and production-grade credit risk management solutions.

Key Takeaways

I. The Problem

AI Is Generating Activity. Not Outcomes.

Fintech leaders across the US and UK have declared AI adoption for two years running. Pilots launched. Models deployed. Yet only 39% of financial services firms report measurable profit impact from AI in 2025.¹ Credit decisions are lagging, default rates remain high, and compliance costs are climbing because most fintechs treat AI as a collection of disconnected experiments rather than as a governed system for financial risk management.

The global AI credit scoring market is growing at 25.9% CAGR through 2031.² 75% of UK financial services firms already use AI.³ 73% of US mortgage lenders cite operational efficiency as their top AI goal.⁴ Yet the gap between adoption and profit has never been wider. Profit in lending demands decision-making that is faster, more accurate, more inclusive, and audit-ready – simultaneously. That requires fintech software development services built around a production engineering system, not a standalone model.

Three structural failures cause most AI credit risk deployments to stall:

- Model Drift: AI credit scoring models degrade silently as borrower behaviour shifts. Without automated drift detection in your credit risk software, accuracy loss shows up in default rates months before anyone identifies the cause.

- Regulatory Explainability: CFPB adverse action notices and FCA Consumer Duty both require specific, traceable decision rationales. Credit scoring models not built with explainability cannot produce these retroactively, creating immediate enforcement exposure.

- Sandbox-to-Production Gap: Models that perform in testing behave differently in live environments. Without an AI-native SDLC, this gap stalls the entire loan underwriting process by months.

II. How Systango Solves It

Introducing the Systango AI-Native Production Framework™

The model is rarely the problem. The engineering system around it always is. The Systango AI-Native Production Framework™ is a three-plane architecture AI-Native SDLC, Data Intelligence Layer, and Governance Plane that converts AI credit risk scoring from a cost centre of experimentation into a governed, profitable production system.

Plane 01 — AI-Native SDLC

Treats intelligence as a first-class engineering product. Model versioning, experiment tracking, and deployment gates enforcing explainability and compliance checks are built into every sprint. Eliminates the sandbox-to-production gap that causes loan underwriting software to fail in live environments. Every model ships with a defined SLA, a monitoring threshold, and a rollback gate.

Plane 02 — Data Intelligence Layer

Unifies bureau data (FICO/Experian US; Equifax/TransUnion UK), open banking feeds under PSD2, behavioural signals, cash flow indicators, and alternative data into one governed feature store enabling true credit risk analysis across all signal types. Real-time data freshness means credit decisions run on signals that are seconds old, not hours. Column-level data lineage automatically satisfies CFPB adverse action requirements and FCA Consumer Duty obligations, functioning as a complete financial risk management software layer not a bolt-on.

Plane 03 — Governance Plane

SHAP-based explainability, decision logs, and model lineage are embedded in every production decision not produced on regulatory request. This is the standard that risk management software for banks must meet in 2025. Bias monitoring runs continuously. Audit-ready reporting for CFPB, FCA, GDPR, and EU AI Act is available from day one. Compliance cannot be retrofitted it must be engineered in.

What the Framework Delivers

• Multi-signal creditworthiness engines – bureau + open banking + behavioural + alternative data, enabling advanced credit risk modelling beyond bureau-only inputs.

• Explainable AI (XAI) by design – SHAP-attributed decisions meeting FCA and CFPB standards natively, making every credit risk assessment fully traceable.

• Dynamic drift detection and automated retraining credit scoring software – stays accurate as borrower behaviour evolves.

• Alternative data integration – unlocking thin-file, gig economy, and self-employed borrowers invisible to traditional credit risk assessment methods.

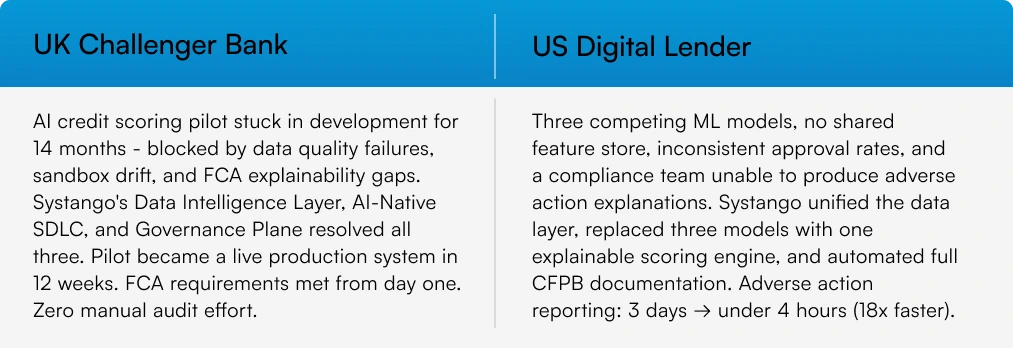

III. Real-World Results

Governed AI credit risk scoring is not a future-state ambition it is already delivering measurable outcomes for lenders who have moved beyond experimentation. The results below reflect what production-grade, multi-signal credit risk systems achieve when explainability, data integrity, and compliance are engineered in from the start. These are not pilot metrics. They are the operational benchmarks your credit risk infrastructure should be held to.

IV. Expected Business Outcomes

What Governed AI Credit Risk Scoring Actually Delivers

The business case for governed AI credit risk scoring is not theoretical it is measurable across five dimensions that matter directly to lending profitability and regulatory standing.

- Higher approvals, fewer defaults. Upstart’s AI model approves 44% more borrowers than traditional FICO-based models while simultaneously reducing defaults demonstrating that multi-signal credit risk modelling does not trade off inclusion against risk. Governed credit risk modelling makes this repeatable at scale.⁵

- Decisions in seconds, not minutes. Lenders using traditional loan underwriting software typically approve in minutes. Systango’s real-time data pipelines deliver credit decisions in seconds without compromising compliance at any point in the workflow.

- Analyst productivity gains of 20–60%. According to McKinsey, AI-assisted credit workflows using agentic multi-agent systems drive productivity gains of 20 to 60% for credit analysts, alongside approximately 30% faster credit decision-making freeing senior analysts for judgment-intensive work rather than data gathering.⁶

- Expanded portfolio without expanded risk. Alternative data integration unlocks thin-file, gig economy, and self-employed borrowers who are permanently invisible to bureau-only credit risk assessment. This expands the addressable lending market without a proportional increase in default exposure.

- Compliance confidence from day one. CFPB, FCA, GDPR, and EU AI Act standards are met at the point of deployment not retrofitted after the fact. Adverse action documentation is automated, and regulatory review costs are reduced significantly.

Systango vs. The Alternatives

V. About Systango

Systango is a publicly listed AI-native digital engineering services company. We help regulated fintechs and lenders move from AI experimentation to production-grade credit risk management transforming how software is built through AI-native SDLC and a governance-first approach to financial risk management. From funded startups to enterprises like Google and Cisco, we are our customers’ technology partner AI-native by design, governance-first by principle, outcome-accountable by default.

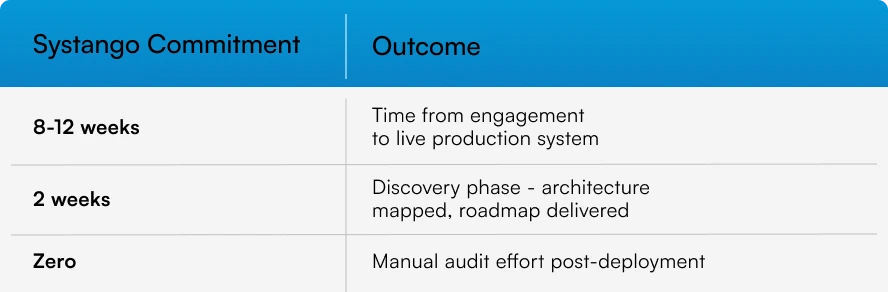

Ready to Move from AI Experimentation to AI Performance?

In 30 minutes, we will map your current credit risk software architecture, identify your FCA, SEC & CFPB compliance gaps, and show you exactly where the Framework moves your numbers.